Channel: Veritasium

How A Random System Can Actually Be Predictable

The Signal

Louis Bachelier, an early 20th-century mathematician, pioneered the use of probability to model financial markets by drawing a direct analogy between stock price movements and the physics of diffusion. He framed the future of a stock price as a random walk, mirroring the behavior of particles forming a normal distribution on a Galton board, and observed that this process follows the same heat equation identified by Joseph Fourier in 1822.

The Case

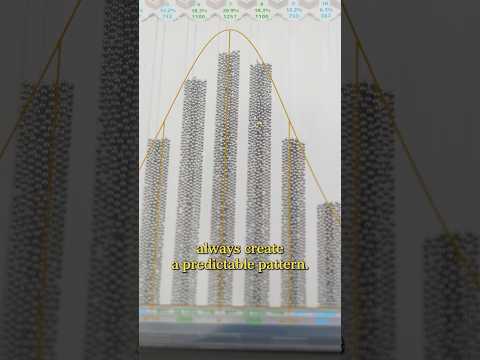

- The Galton board uses a triangle of pegs to force ball bearings into 50/50 left-or-right choices at each level; while any single particle's path is unpredictable, the aggregate collection consistently produces a normal distribution.

- Bachelier treated stock price fluctuations as a time-evolving random walk, where every additional time step acts like a new layer of pegs on a board, causing the range of possible future prices to widen over time.

- By recognizing that the math behind diffusing heat—the radiation of flow from hot to cold regions—mirrored his financial models, Bachelier labeled his insight the "radiation of probabilities."

- The transcript asserts that Bachelier is the primary "pioneer" of this mathematical approach and attributes the discovery of the heat equation to Joseph Fourier in 1822; however, these historical claims are provided without independent evidentiary support or documentation.

The 1 Minute Signal Take

The video offers a clean, entry-level explanation of how the math of physics crossed over into finance, but it is an intuitive analogy rather than a rigorous or historical proof. Skip it if you are looking for a deep technical or historical analysis; watch it only if you need a quick, visual-minded orientation on how random walks underpin market modeling.

Time saved:

Channel: Veritasium